How AV Integrators Can Stop Margin Erosion in Project Proposals

Sahil Dhingra

Published 16 June 2026

Most AV firms treat margin erosion as a project delivery problem. The job runs long. A programmer bills more hours than estimated. Freight comes in higher than quoted. By the time finance flags the numbers, the damage is done.

That thinking is incomplete. Margin erosion in AV most often begins before the first cable is pulled. It starts inside the proposal, when equipment cost, labor effort, shipment, discounts, and profitability are not reviewed together before the quote goes out.

According to AVIXA’s IOTA 2025 report, pro AV revenue is set to grow from $332 billion in 2025 to $402 billion by 2030. More revenue means more proposals. More proposals means more quoting. And more quoting means more chances for pricing mistakes to slip through. Growth does not fix a broken quoting process. It exposes it faster. The firms that benefit most will not just be the ones winning more work. They will be the ones pricing it right.

The firms that will win over the next five years are not just the ones that close more deals. They are the ones that know their proposal numbers before they hit send.

Key Takeaways

- Margin erosion does not start on the job site. It starts in the quote.

- Labor is where most AV firms bleed profit. Quote every role separately. Never use a lump sum.

- A discount without margin visibility is a guess. The sales team needs to see gross profit impact before the price drops.

- Total margin hides the real story. Equipment and labor must each have their own column.

- Markup is not margin. A 25% markup is a 20% margin. That gap compounds fast across a full year of proposals.

- Freight and tax are not line items to add later. On big jobs, freight alone can hit 4-6% of total project cost.

- A complete proposal is not the same as a profitable one. The approval process should check both.

- All cost variables need to be in one view before the quote is sent. Not in three tabs, not in two systems.

The all-in-one solution for your Audio Visual (AV) Project Design & Documentation needs

Transform your audio-visual experience with XTEN-AV.

No Credit Card required

What Is Margin Erosion in AV Project Proposals?

Margin erosion in AV project proposals happens when expected profit decreases before or during project delivery because costs, discounts, labor, shipment, tax, or scope changes are not fully reflected in the proposal price. It turns a quote that looks profitable into a project that delivers weaker-than-planned margin.

Markt-Pilot defines margin erosion as a slow drop in profit caused by rising costs or poor pricing decisions. That explains what happens. It does not explain why.

In AV, the cause is usually simpler. Proposals are built across multiple line items: displays, racks, cabling, DSP units, labor by role, freight, taxes, discounts. When those numbers are entered, reviewed, and approved in isolation, the total margin picture is never visible until it is too late.

The proposal becomes the financial baseline for the entire project. Whatever margin is locked into the quote is the margin the company is working with. That is why the pricing stage is where margin protection must begin.

Why Do AV Integrators Lose Margin Before the Project Even Starts?

AV integrators lose margin before a project starts when proposal pricing is based on incomplete cost visibility. Missing shipment costs, weak labor estimates, outdated equipment pricing, unclear tax treatment, and aggressive discounts can reduce profit before the client signs, before the installation team even receives the project file.

Think about how most AV proposals are actually built. A sales engineer pulls equipment from a price list that may be weeks or months old. Labor hours are estimated from memory or a rough template. Freight is either omitted or added as a flat-rate guess. Tax is handled separately by finance, sometimes after the quote is approved.

Nobody is doing this badly on purpose. These are time pressures, disconnected systems, and habits that formed when projects were simpler. But the gap between what a proposal assumes and what a project actually costs is where margin disappears.

Tacton’s research on CPQ margin erosion in manufacturing describes the same dynamic: margin loss often starts in quoting when teams use outdated costs, price too low, or apply discounts without guardrails. The parallel in AV is direct.

Take a $150,000 conference room project. The numbers look fine on paper.

- Displays, DSPs, switchers, racks, mounts, and cabling cost $78,000. They sell for $102,000.

- Labor, design, installation, DSP tuning, and control programming costs $22,000 and sells for $38,000.

- Freight is $3,000. Gross margin sits around 26%.

That looks like a solid deal.

Then three things happen:

- Sales applies a 5% discount to close the deal.

- DSP tuning and control system programming require 32 more hours than estimated.

- Freight increases by $1,500 due to supplier changes.

Nothing catastrophic happened. No major scope change occurred. Yet the project margin can easily fall below 18%.

This is why margin erosion rarely arrives as a single event. It is usually the accumulation of small pricing decisions that were never reviewed together.

What Causes Margin Erosion in AV Proposals?

The biggest causes of AV proposal margin erosion are poor cost estimates, labor underestimation, discounting without margin visibility, missing shipment or tax costs, scope assumptions, outdated vendor pricing, and disconnected proposal reviews. These issues reduce profit because the proposal does not reflect the real cost to deliver the system.

Labor Underestimation

Labor is the fastest route to margin loss in AV. Commercial Integrator notes that AV professionals need to know their true burdened labor rate and apply data-driven cost tracking to price work accurately.

Most integrators underestimate labor for one reason: they quote based on best-case scenarios. The boardroom install goes smoothly. The programmer finishes on schedule. The commissioning is clean. But hotel deployments and command center projects rarely behave that way. Site access delays, rework, and extra client training sessions are real costs that rarely appear in the original proposal.

The AV project cost estimation checklist approach is to break labor into specific roles: design hours, CAD and engineering, rack build, cable pull, installation, programming, commissioning, project management, site visits, and client training. Quote each separately. A single blended labor rate across a complex project hides the true cost.

There is another number most teams ignore. A technician earning $35 an hour does not cost the company $35 an hour. Payroll taxes, benefits, vehicle costs, insurance, and training push that number much higher. That is the burdened rate. Quote labor without it and the margin is wrong before anyone picks up a tool.

Equipment Cost Changes

A DSP specified six weeks ago may now carry a manufacturer price increase. It may have a longer lead time. It may need a substitute model entirely. Display pricing shifts with supply and import costs. Switching equipment gets discontinued mid-project.

If the proposal is built from a price list that is 60 or 90 days old, the cost-to-company figure is wrong before the quote leaves the building. The client never sees that change. The integrator absorbs it.

Discounting Without Approval Thresholds

Sales teams discount to win. That is a legitimate tool. The problem is that a 5% discount on a $200,000 AV proposal is a $10,000 hit to gross profit. If the discount is applied without the team seeing how it affects total margin, labor recovery, and final price simultaneously, there is no way to know whether the deal is still worth taking.

Shipment and Logistics Gaps

Freight is easy to overlook because it feels secondary. It is not. Shipping large displays, LED walls, equipment racks, and AV infrastructure across a hotel or campus deployment is not cheap. White glove delivery alone adds cost.

On large jobs, freight can reach $4,000 to $8,000 or more. If that number is added late, guessed, or left out entirely, the margin is already weaker than it looks.

Tax and Final Price Mismatch

Tax treatment varies by client type, project location, and contract structure. When tax is reviewed separately from the rest of the proposal or added after the sell price is locked, the final client-facing number and the internal cost view stop matching. That gap shows up as a margin surprise later.

Scope Gaps Between Design and Proposal

When the design scope and the proposal scope are not aligned, the proposal is pricing a project that does not match what the AV system drawing actually requires. Extra cable runs, additional rack units, or scope changes that happened during design but were not updated in the quote create the conditions for a loss.

How Do Discounts Quietly Reduce AV Proposal Profit?

Discounts reduce AV proposal profit when sales teams lower the client price without seeing how the change affects gross margin, equipment profit, labor recovery, tax, shipment, and final price together. A discount can help win the job but without margin visibility, it can quietly turn a healthy proposal into a weak-margin project.

Discounts are not the enemy. The lack of visibility into what a discount actually does to profitability is.

Here is a simple example from a mid-size AV project:

Proposal Item | Before Discount | After Discount |

Equipment sell price | $80,000 | $76,000 |

Labor sell price | $30,000 | $30,000 |

Shipment | $3,000 | $3,000 |

Discount applied | $0 | $4,000 |

Gross profit impact | Healthy | Reduced |

Here is the actual math. Equipment costs $62,400 and sells for $80,000. That is a 22% margin. Apply a $4,000 discount and the sell price drops to $76,000. Margin falls to 17.9%. That is before any labor overrun or freight increase. A single discount, approved without visibility, cost four margin points.

The discipline is not saying no to discounts. It is making sure the person approving the discount can see the gross margin, final price, and profit figure in the same view before they decide.

Why Is Labor Underestimation One of the Fastest Ways to Lose AV Margin?

Labor underestimation erodes AV margin because installation, engineering, programming, commissioning, and project management hours are hard to recover once the proposal is approved. Underprice labor in the quote, and every extra hour chips away at profit, even when equipment margins look fine.

Equipment margin is easy to see. A display costs $2,000 and sells for $2,600. The math is right there. Labor is different. It depends on accurate hour estimates, real burdened rates, and phase-by-phase planning. Most teams skip that detail.

Most margin loss in AV does not come from equipment discounts. It comes from programming budgeted for three days that takes five. A commissioning visit that needs two extra site trips. Project management hours that never made it into the quote because someone called them overhead.

On any project above $50,000, break labor out by role and phase. Design hours. CAD and documentation. Rack build. Cable pull. Installation. Programming. Commissioning. Project management. Site visits. Client training. Price each one separately.

Quoting one labor number across a complex hotel AV rollout is not a strategy. It is a guess.

How Do Equipment Margins and Labor Margins Differ in AV Proposals?

Equipment margin comes from the difference between product cost and product sell price. Labor margin comes from the difference between the internal cost of labor and the labor price charged to the client. AV integrators need to review both separately, because one can mask weakness in the other.

This is one of the most overlooked points in AV proposal pricing. A proposal can show a total gross margin of 28% and still be losing money on labor. How? Because strong equipment margin offsets weak labor recovery in the blended number.

D-Tools has reported that integration companies show different margin patterns across sectors, with equipment and labor contributing unevenly across residential, commercial, and security projects. That finding is consistent with what most AV business owners see in their own numbers.

The only way to catch this problem is to look at equipment cost, sell price, gross margin, and profit in one column and labor cost, sell price, gross margin, and profit in another. Total margin should be a summary, not the primary view.

What Is the Difference Between Margin Pricing and Markup Pricing in AV Proposals?

Margin pricing calculates profit as a percentage of the final sell price, while markup pricing adds a percentage above cost. The two methods produce different profit results. Confusing markup with margin is a common error in AV sales, and it makes proposals look more profitable than they actually are.

Here is the clearest example:

An item costs $1,000 and is sold for $1,250.

- Markup = 25% (profit divided by cost)

- Margin = 20% (profit divided by sell price)

Both numbers describe the same transaction. But 25% sounds healthier than 20%. If a sales director sets a company-wide target of “25% margin” and their team is actually calculating markup, the real margin on every project is lower than the target.

That gap shows up in every deal. Across a full year of proposals, it is not a small number.

Pick one method. Write it down. Train the sales team on what it actually means. Then use it on every proposal, every time.

How Do Shipment, Tax, and Final Price Gaps Affect AV Project Profitability?

Shipment, tax, and final price gaps affect AV profitability because they change what the company actually pays and what the client actually sees. If these values are reviewed separately from equipment and labor pricing, the proposal can lose margin without anyone noticing during approval.

Shipment and tax tend to get treated as administrative line items, things finance handles after the main quote is built. That habit is costly. For a hospital AV deployment or a campus-wide classroom installation, equipment freight alone can represent 4–6% of total project cost. As XTEN-AV’s AV project budget tracking guidance makes clear, procurement cost and vendor pricing variance need to be visible at the proposal stage, not after the purchase orders go out.

Tax compounds the issue. Depending on client type, government, nonprofit, commercial and project location, applicable tax rates and exemptions vary. If the proposal is built with one tax assumption and the actual invoice reflects another, the margin number is wrong in ways that can be difficult to reconcile later.

The fix is structural. Shipment amount, discount on freight, tax rate, and final client-facing price should all be visible in the same pricing view as equipment and labor, not in a separate spreadsheet tab added the day before the quote goes out.

How Can AV Sales and Finance Teams Catch Margin Erosion Before Quote Approval?

AV sales and finance teams can catch margin erosion before quote approval by reviewing equipment cost, labor cost, shipment, tax, discount, final price, gross margin, markup, and profit in one pricing workflow. The goal is to identify profit leakage before the client receives the proposal.

Most AV firms have a proposal review process. The problem is that the review checks completeness. Did the scope include everything? not profitability. A complete proposal and a profitable proposal are not the same thing.

Before any AV proposal is sent, the team should be able to answer these questions:

- Is equipment cost updated from current vendor pricing?

- Is labor priced by role and phase, not as a lump sum?

- Is shipment included as a concrete estimate, not a placeholder?

- Is tax visible and calculated correctly for this client type?

- Is the discount impact visible in terms of gross margin and profit, not just total price?

- Is margin calculated correctly not confused with markup?

- Is the final client price aligned with the cost to the company?

- Has finance or management reviewed and approved any low-margin exceptions?

That is a simple checklist. The harder part is having a system where all of those variables are in the same place at the same time, not spread across a CRM, a spreadsheet, an email thread, and a separate finance review.

Still checking AV proposal margins in spreadsheets?

See how XTEN-AV gives sales and finance teams real-time visibility into equipment cost, labor cost, discounts, shipment, tax, margin, markup, and final price, before the proposal goes out.

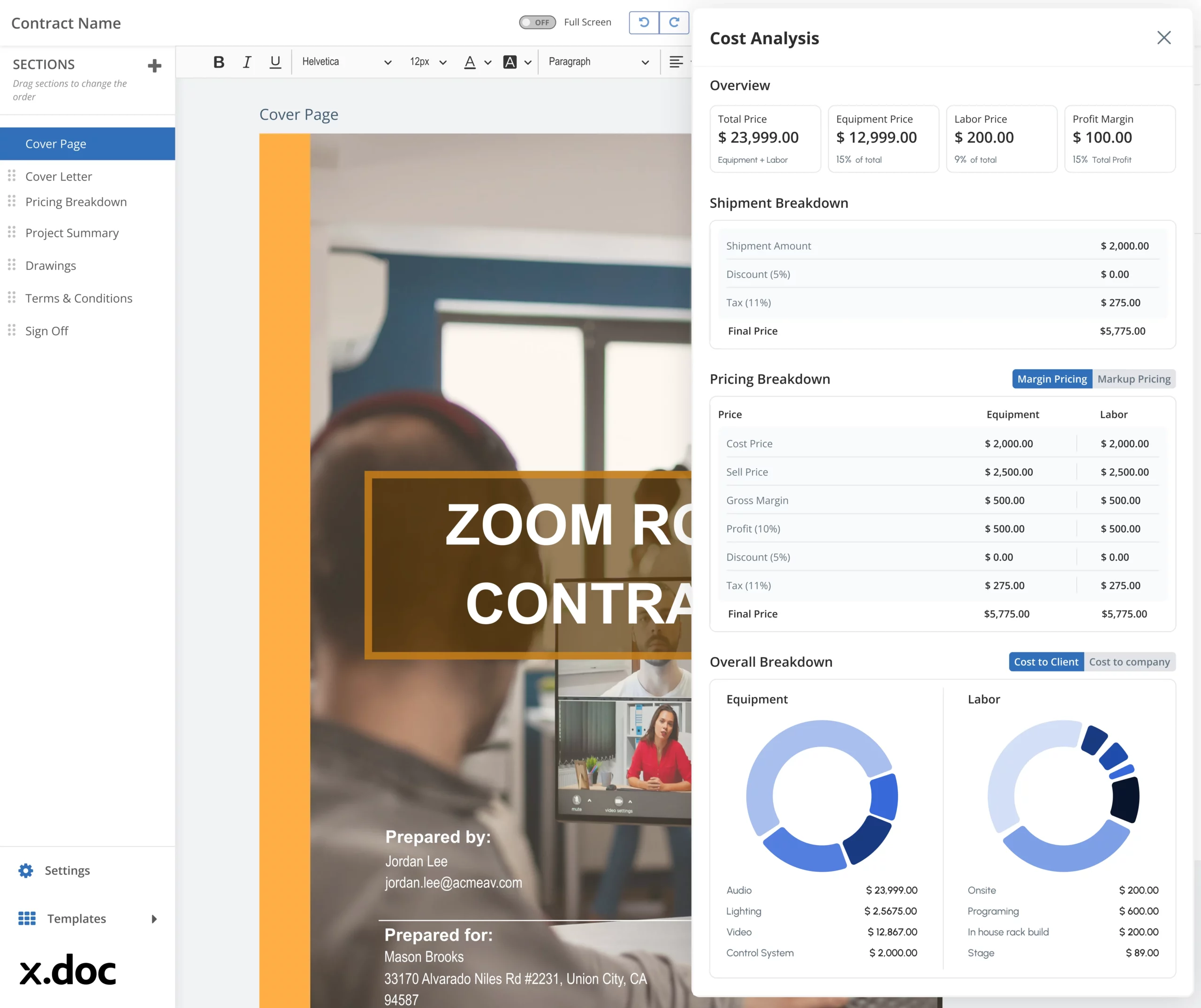

How Does XTEN-AV x.doc Help AV Teams Protect Proposal Margins?

Most AV teams build the quote in one place and check profitability in another. By the time the numbers are reviewed, the proposal is already out.

Audio visual (AV) proposal software like x.doc puts the cost analysis inside the proposal itself. Equipment pricing, labor pricing, shipment, tax, discount, gross margin, markup, and profit are all visible in the same panel where the quote is built. Sales does not have to wait for finance. Finance does not have to chase the sales team. Both see the same numbers at the same time.

On the equipment side, every line item shows cost price, sell price, gross margin, profit, discount, tax, and final price. Displays, DSPs, switchers, racks, each one tracked separately. On the labor side, the same view applies. Cost by role, sell price, gross margin, and profit. Neither column hides behind the other.

The Margin vs Markup toggle fixes one of the most common pricing mistakes in AV sales. Switch between both methods and see exactly what the profit looks like under each. That is harder to get wrong than a standard set in a sales meeting and forgotten by Friday.

Freight, tax, and final price sit in the same view. Not a separate tab. One click on the Cost to Client vs Cost to Company toggle and the full picture is there.

For AV firms looking at AV project cost estimating software, the question is not which tool has the most features. It is which one shows the margin before the quote goes out, not after the job is closed.

Every proposal locks in future project profitability. Make sure you can see equipment margin, labor margin, shipment cost, and discount impact before the quote reaches the client.

Book a demo with XTEN-AV and see how it works.

The all-in-one solution for your AV needs

Transform your audio-visual experience with XTEN-AV.

No Credit Card required

Audio Visual System Design Mastery + Winning Proposals = 10x Productivity!

- ✔ Automatic Cable Labeling & Styling

- ✔100+ Free Proposal Templates

- ✔ Upload & Create Floor Plans

- ✔1.5M Products from 5200 Brands

- ✔ AI-powered ‘Search Sense'

- ✔Legally Binding Digital Signatures

FAQ's

AV margin erosion is when an AV project makes less profit than planned. It happens when the proposal price does not cover all the real costs. Labor, equipment, discounts, shipment, or tax can each eat into profit. Most firms only notice it after the project is done.

The most common cause is labor underestimation. Teams quote fewer hours than the job actually needs. Outdated equipment pricing, vendor costs change, but the price list does not. Discounts hurt too, when no one checks how they affect total margin. Missing freight costs and unclear tax treatment add to the problem. The real issue is that no one looks at all these numbers together before the quote goes out.

Check every cost before the quote is sent. That means equipment cost, labor by role and phase, shipment, tax, discount impact, and final price, all in one view. A spreadsheet split across tabs does not work. Sales and finance need to see the full margin picture at the same time, in the same place.

Labor hours are hard to recover once the quote is approved. If programming is underpriced by 20 hours, those hours still get worked. The project absorbs the cost. Equipment margin can look fine while labor quietly erases the profit. That is why labor must be reviewed separately, not buried inside a total margin number.

Margin is profit as a percentage of the sell price. Markup is profit as a percentage of the cost. Same transaction, different numbers.

An item costs $1,000 and sells for $1,250. Markup is 25%. Margin is 20%. Neither is wrong. But if the sales team targets “25% margin” and calculates markup instead, every proposal in the pipeline is less profitable than it looks.

XTEN-AV puts equipment cost, labor, discounts, tax, shipment, and profit in one view. Sales sees the client price. Finance sees the delivery cost. Both teams check the same numbers before the quote goes out.

Explore more by topic

AV Design Mastery + Winning Proposals = 10x Productivity!

- Automatic Cable Labeling & Styling

- 100+ Free Proposal Templates

- Upload & Create Floor Plans

- 1.5M Products from 5200 Brands

- AI-powered ‘Search Sense'

- Legally Binding Digital Signatures

No Credit Card Required

Related Blogs

-

- Posted by Sahil Dhingra

Audio Visual 5 Best Speaker Placement Calculators for Commercial AV Projects in...

-

- Posted by Sahil Dhingra

Audio Visual How XTEN-AV Helps Manage AV Service Calls After Installation Sahil...

-

- Posted by Sahil Dhingra

Audio Visual Field Service Metrics for AV Integrators Sahil Dhingra Published 20...